According to the “2025 Global Risks Report” released by the World Economic Forum (WEF) on January 15, 2025, environmental risk is the most severe risk factor the world will face in the next 10 years, and climate change has become an important issue of global concern in recent years. Meanwhile, the sustainable transformation of enterprises has shifted from being a bonus requirement in the past to a mandatory requirement for sustainable development.

In order to enhance the operational resilience and international competitiveness of Taiwanese enterprises, regulatory authorities have actively promoted the sustainable transformation of the capital market through policy guidance in recent years. At the same time, as the central hub of the capital market, the TWSE expects to gradually improve the transparency of ESG information to allow more funds to flow into companies with better sustainability performance, ultimately achieving a win-win situation where both corporate value and sustainability performance are enhanced.

The following is the development process of sustainability information disclosure in Taiwan in recent years:

I. Improvement in Both Quality and Quantity of the Sustainability Report

The Corporate Social Responsibility (CSR) Report was initiated in 2014. In conjunction with the release of the “Corporate Governance 3.0 – Sustainable Development Roadmap” (“Corporate Governance 3.0”) initiative by the Financial Supervisory Commission (FSC) in 2020 to promote the sustainable development of the capital market, the report was officially renamed the Sustainability Report in 2022. At the beginning, only specific industries such as the food industry with the catering revenue accounting for more than 50% of the total operating revenue, the chemical industry, the financial and insurance industry, as well as enterprises with a paid-in capital exceeding NT$10 billion were required to prepare the Sustainability Report. After nearly a decade of policy evolution and in response to the increasing demand for ESG information by international investors and industry chains, the FSC released the “Action Plan for Sustainable Development of TWSE/TPEx Listed Companies (2023)” (the “Action Plan”) in 2023 to further expand the coverage of the Sustainability Report, and required that all TWSE/TPEx listed companies prepare the Sustainability Report from this year (2025) onwards, and file a declaration and disclose the report in the Sustainability Report Area under the “Enterprise ESG” section of the Market Observation Post System.

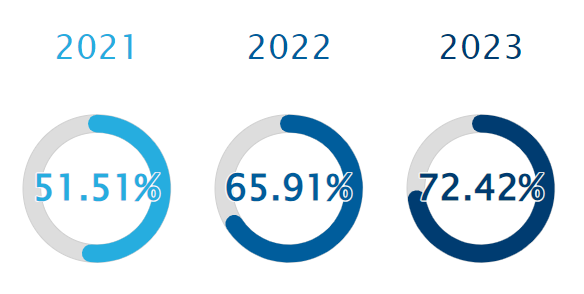

Since the FSC promoted the preparation of the Sustainability Report by TWSE listed companies in 2014, the number of companies issuing the report has been increasing year by year. At the end of 2024, 722 listed companies issued their Sustainability Report for 2023, accounting for more than 70% of all TWSE listed companies.

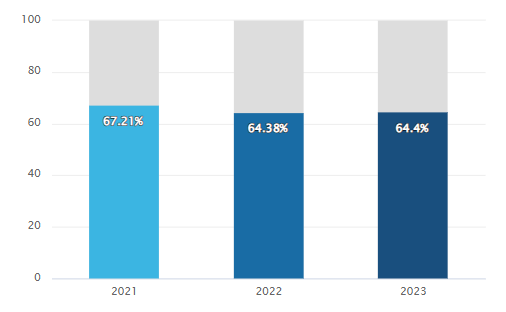

Other than mandatory disclosure of the Sustainability Report, the credibility of its contents is one of the issues of concern to external parties. The TWSE revised the “Regulations for the Preparation and Declaration of Sustainability Report by TWSE Listed Companies” (the “Regulations”) in 2021 to expand the scope of third-party verification, requesting companies in industries including food, chemicals, and financial services and insurance to have their respective sustainability indicators assured. At the same time, the TWSE actively encourages other companies to have the contents of their sustainability reports assured in order to enhance the reliability of their sustainability information. The third-party verification of the Sustainability Report by CPAs or professional certification bodies can ensure the reliability of the information presented in the report and improve its quality. The number of listed companies that issued the 2023 Sustainability Report and obtained third-party verification in 2024 is 465, accounting for 64.4% of the total number of companies that prepared the report, with about 80% of them obtaining the verification voluntarily.

II. Strengthening Sustainability Information Disclosure in Accordance with International Standards

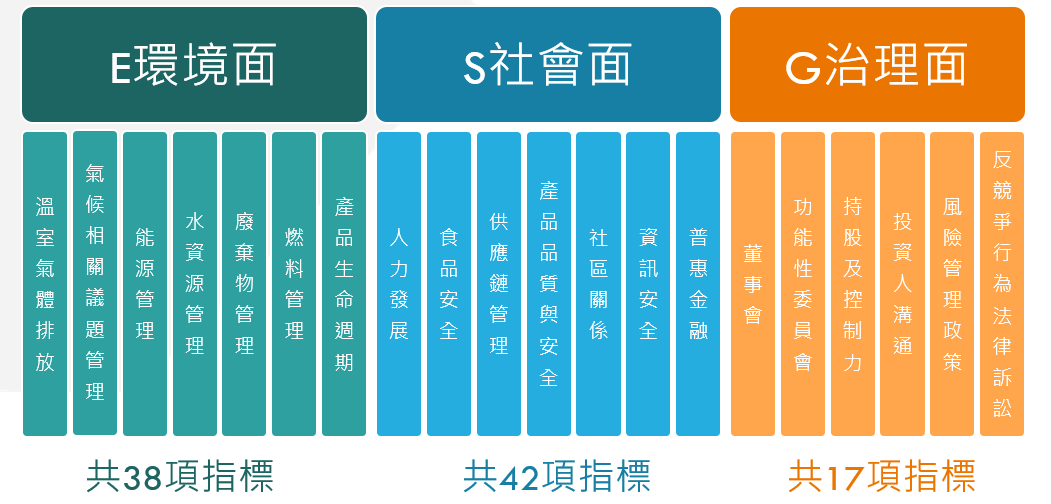

In compliance with the specific promotion measures of Corporate Governance 3.0, the TWSE further required in the Regulations that in addition to referring to GRI Standards for report preparation, companies may refer to SASB Standards to disclose sustainability indicators corresponding to their industry categories. SASB divides the market into 11 major industries and 77 businesses, and companies shall disclose their corresponding sustainability indicators based on their industry categories to enable indicator disclosure to have financial impact materiality, investor decision relevance, consistency, and comparability, in order to make it easier for users to apply sustainability information for comparison among related industries or businesses, assist stakeholders in understanding the performance of enterprises in sustainability issues, and facilitate investment decisions.

To facilitate inter-industry comparisons among domestic companies, the TWSE referred to SASB Indicators and took into account the characteristics of domestic industries in its formulation of Local Industry Sustainability Disclosure Indicators (Appendix 1) in the Regulations, requiring that 14 industries including food, chemical, financial and insurance, cement, semiconductor industry, etc. categorized by the local capital market to include the aforementioned Appendix 1 in the Sustainability Report in accordance with regulations to strengthen the disclosure of industry-specific sustainability indicators.

In addition, in response to the international attention to climate change issues, the TWSE referred to the framework of the Task Force on Climate-related Financial Disclosures (TCFD) established by the Financial Stability Board (FSB) and formulated “Appendix 2 – Climate Related Information of TWSE Listed Companies” in the Regulations, requiring TWSE listed companies to disclose in the Sustainability Report climate change related monitoring and governance as well as risks and strategies, and provide specific data and targets accordingly.

III. Promoting TWSE Listed Companies’ Greenhouse Gas Reduction and Information Disclosure

To support the government’s net-zero carbon emission target by 2050, the FSC released the “Sustainable Development Roadmap for TWSE/TPEx Listed Companies” on March 3, 2022, and promotes the phased completion of greenhouse gas inventories by 2027 and greenhouse gas inventory assurance by 2029 for all TWSE/TPEx listed companies, in order to ensure the continuous improvement of the sustainable development (ESG) ecosystem. According to statistics, as of the end of 2024, 792 companies (641 of which made voluntary declarations) have disclosed their Scope 1 (direct emissions) and Scope 2 (indirect energy emissions) greenhouse gas inventory data.

To achieve the goal of net-zero transformation in the capital market, the Action Plan released by the FSC in 2023 further encourages TWSE/TPEx listed companies to establish carbon reduction targets, strategies, and specific action plans. In terms of information disclosure and operational measures, the “Regulations Governing Information to be Published in Annual Reports of Public Companies” requires companies to disclose their greenhouse gas inventory and assurance information in different phases, and to disclose relevant information from 2025 onwards in phases according to their respective capital sizes and industry categories. In addition, the FSC encourages companies to disclose their 2030 carbon reduction targets, strategies, and action plans, using the year of inventory information disclosure in their consolidated financial report as the base year. This disclosure is awarded a bonus point in the 2025 Corporate Governance Evaluation.

IV. Developing ESG Indicators for Consistent Disclosure

In order to make all TWSE listed companies gradually emphasize sustainable management, and in response to the increasing market demand for comparable sustainability information, the TWSE revised the “Information Declaration Measures” to require TWSE listed companies to report the “Corporate Environmental, Social and Governance (ESG) Information” by the end of June each year starting from 2022. In response to the rapidly developing ESG topics, after reviewing the disclosure contents of the annual report and the sustainability report in 2024, the TWSE encourages companies to disclose important industry-specific sustainability indicators by expanding the sustainability information to be declared by TWSE listed companies from 7 important topics to 20 important topics, and the number of ESG indicators from 29 to 97, in order to enhance the transparency of the overall market’s sustainability information.

Conclusion

In the face of the increasing emphasis of the global market on sustainable development topics, Taiwanese companies have demonstrated high operational resilience and competitiveness amid the wave of sustainable transformation. The TWSE will continue to comply with the regulatory authorities’ policies, guide TWSE listed companies to follow the sustainable development roadmap for completion of greenhouse gas inventory and assurance, comply with IFRS International Sustainable Disclosure Standards, and establish internal controls for corporate sustainability information, in order to enhance the credibility and transparency of sustainability information. By working together with stakeholders, we can establish a solid and resilient ESG ecosystem, and achieve the sustainable development goals of “environmental sustainability, social well-being, and orderly governance.”