Overview of IPO Underwriting Placement Methods

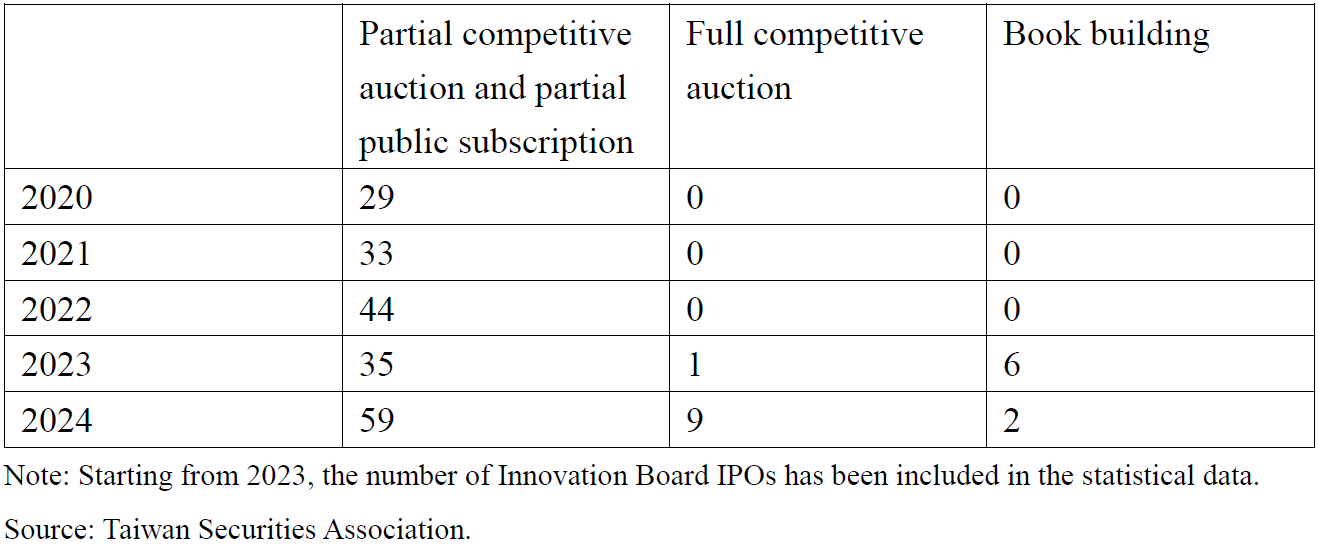

The underwriting placement of initial public subscriptions (IPOs) for TWSE/TPEx listing in Taiwan may be handled through methods such as full competitive auction, full book building, partial competitive auction and partial public subscription, and partial book building and partial public subscription in accordance with the “Taiwan Securities Association Rules Governing Underwriting and Resale of Securities by Securities Firms.” In order to enhance the fairness and rationality of the underwriting system, the regulatory authorities have promoted the use of competitive auctions as a priority for IPOs since 2016. Due to its good results and deep market recognition, the vast majority of IPOs has adopted a combination of competitive auction and public subscription in recent years to handle underwriting placement, and full competitive auction or book building has been chosen only for some Taiwan Innovation Board IPOs.

Reason for Shortening the Timeline from IPO Pricing to Listing

In the past, the base date for the underwriting placement timeline of partial competitive auctions and partial public subscriptions was the bid opening date T, on which the underwriting price was determined. The listing date was T+10, which means that the interval between the determination of the IPO listing price and the actual completion of the share listing for trading in the securities market was as long as 10 trading days. The main reason is that after the bidding and bid opening of the competitive auction, there is still the subsequent handling of the public subscription. In order to confirm the IPO underwriting price, which serves as a reference for investors participating in the subscription and as a calculation basis for brokers to withhold the subscription cost, a series of public subscription procedures must be initiated after the completion of the bidding and bid opening of the competitive auction. This results in a longer overall underwriting placement period.

Compared with those of major international securities markets, the above-mentioned IPO timeline not only has a longer operating period which is not conducive to the fundraising efficiency of the issuing company, but more importantly, investors participating in the competitive auction must bear greater uncertainty, thereby weakening the price discovery function of the securities market. Because the final point at which investors may make bidding decisions based on market information is the bidding deadline T-2 for the competitive auction, and considering the possibility of new information affecting market prices, there may be a significant gap by the listing date T+10 between the market price at which investors may sell and the winning bid price. Therefore, considering that bidders must bear the uncertainty, for risk avoidance, their bidding price will tend to be conservative which may lead to an increase in the discount of the winning bid price, and thereby a relative decrease in the final fundraising amount for the issuing company.

Shortened Timeline of the New Underwriting Placement System

In order to accelerate the underwriting placement process for IPO cases involving a partial competitive auction and a partial public subscription, the TWSE proposed to the regulatory authority, the Financial Supervisory Commission and the Securities and Futures Bureau, in 2022, to bring forward the public subscription operation in parallel with the competitive auction. After obtaining approval from the regulatory authorities in 2023, the TWSE jointly discussed the adjustment plan and supporting operational plans with the Taiwan Securities Association and decided to bring forward the start date of the public subscription from T+2 to T-1. After the adjustment, the IPO pricing and listing timeline has been shortened from T+10 to T+7.The relevant underwriting regulations were revised by the Taiwan Securities Association on June 27, 2024, and the TWSE assisted in the adjustments to the computer systems and securities firm operations. The revised regulations were officially implemented on March 31, 2025.

After the shortening, the key points for the adjusted underwriting placement system for competitive auction and public subscription are as follows:

- The start date of public subscription is brought forward to one day before the bid opening date (T-1).

- The lead underwriter shall publish a “Notice of Competitive Auction and Public subscription” on the bidding start date (T-4), and disclose the provisional underwriting price at a certain multiple of the lowest bidding price of the competitive auction.

- Underwriters shall input the actual underwriting price before 12:30 on the bid opening day (T), and the TWSE shall disclose the actual underwriting price on its website at 13:30 and transmit it to brokers. Brokers shall disclose the actual underwriting price no later than the public subscription deadline (T+1).

- The subscription price that investors should deposit into the bank for the public subscription shall still be based on the actual underwriting price after the bid opening.

- In the event of a natural disaster causing a postponement of the competitive auction, the public subscription shall, in principle, also be postponed; however, the timeline in the underwriting announcement shall prevail.

Benefits of Shortening the Timeline from IPO Pricing to Listing

After the implementation of the new system of partial competitive auction and partial public subscription on March 31, 2025, it is expected that about 50 IPO cases can enjoy the shortened underwriting placement period each year, bringing the following benefits to the securities market:

- The timeline from pricing to listing for IPOs is shortened from T+10 to T+7 to improve the efficiency of underwriting placement operations and accelerate the enterprise’s fundraising timeline.

- The uncertainty that investors face from winning the IPO competitive auction to listing is reduced, allowing them to trade the subscribed shares on the market earlier.

- The uncertainty that investors must bear when participating in competitive IPO auctions is reduced, allowing the pricing results to better reflect the true value of the enterprise. This, in turn, strengthens the competitiveness of the capital market and promotes its long-term development.