Overview of Taiwan’s Securities Lending Market

The securities lending market in Taiwan has developed for over two decades. Since the official launch of the securities lending system by the Taiwan Stock Exchange (TWSE) on June 30, 2003, the market’s institutional framework has gradually evolved and been optimized. Subsequently, in 2006, securities firms and the Taiwan Securities Finance Company were allowed to conduct securities lending transactions independently, providing more diversified channels for securities lending. In 2016, securities firms were further permitted to engage in two-way lending transactions, effectively expanding available securities and enhancing market liquidity. Through these institutional advancements and policy initiatives, the TWSE’s securities lending system and the lending operations of securities firms have gradually developed a complementary relationship, enhancing overall market efficiency and flexibility and laying a solid foundation for the stable development of Taiwan’s securities lending market.

Observing recent market developments, in 2025 the total securities lending transaction value reached NT$13.80 trillion, with NT$11.19 trillion transacted through the TWSE’s securities lending system and NT$2.61 trillion via securities firms, representing a 10.96% increase from the previous year. This marks six consecutive years of growth, indicating sustained expansion in market participation and trading demand.

From a stock perspective, as of the end of 2025, the balance of outstanding loans in the TWSE’s SBL system was approximately NT$1.84 trillion, while the balance in SBL by Brokers was approximately NT$0.57 trillion, totaling NT$2.41 trillion for the overall market, with a year-on-year increase of 32%. This trend demonstrates that, alongside continued growth in transaction volume, outstanding loan balances are also increasing, largely due to the expansion of Taiwan’s total market capitalization in recent years. As the volume of securities available for lending rises correspondingly, securities lending balances grow in tandem, highlighting the strong correlation between the development of the lending market and the overall capital market.

Further analyzing transaction types, in 2025 the TWSE’s SBL system recorded NT$11.19 trillion in lending transactions, predominantly via negotiated loans, which accounted for 98% of the total transaction value, while competitive-bid transactions accounted for only NT$0.24 trillion, or approximately 2%. This structure indicates that the market is still primarily driven by institutional investors’ customized lending needs. Negotiated transactions, offering flexible terms such as rates, duration, and collateral arrangements, better meet the strategic requirements of large investors, making it the dominant transaction mode.

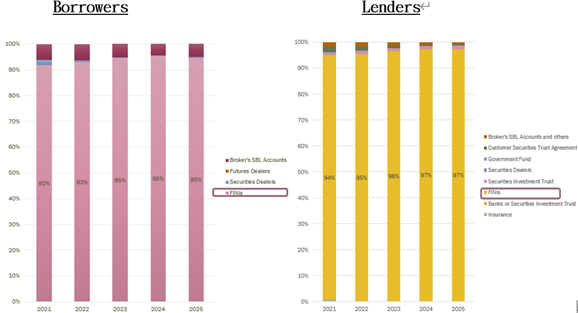

Regarding market participant structure, securities lending serves as an important tool for foreign investors to execute strategic operations in Taiwan’s capital markets, such as hedging, arbitrage, and short selling. Consequently, foreign investors constitute the primary participants in the securities lending market. In recent years, foreign investors’ lending and borrowing transaction values have consistently accounted for over 90% of total market volume, with a gradual upward trend (as shown in Figure 1). This demonstrates the deepening engagement of international capital in the Taiwan market and reflects the increasing functional importance of the securities lending market within the broader capital market.

Existing SBL Related Fees Payment Mechanism and Market Participant Challenges

Under the existing framework, lending-related fees for fixed-price, competitive-bid, and negotiated transactions are paid on the next business day following the return of borrowed securities. As such, the timing of fee payments is closely linked to the settlement of return transactions.

In recent years, with the rapid expansion of the securities lending market, the volume of lending transactions has increased significantly, driving a corresponding rise in return transactions and, consequently, a substantial increase in the frequency of fee calculation, settlement, and payment operations.

Based on empirical statistics, there were a total of 244 trading days in 2025, and on every trading day, borrowers conducted return transactions through the securities lending platform established by the TWSE. The total annual return transaction volume reached 95,846 thousand shares, representing an increase of 12% compared to the previous year, while the total number of return transactions amounted to 208,330, reflecting a year-on-year increase of 13%.Among these, 179,103 transactions, or approximately 86%, were attributable to negotiated transactions, indicating that negotiated lending is the primary driver of return transaction frequency.

Given that the current mechanism initiates fee calculation, settlement, and payment processes immediately after each return transaction, market participants are required to perform such operational procedures frequently in practice, resulting in increased administrative burden.

| Year | Total Number of Return Transactions | Number of Negotiated Return Transactions (%) | Number of Fixed-Price & Competitive-bid Return Transactions (%) |

| 2025 | 208,330 | 179,103 (86%) | 29,227 (14%) |

| 2024 | 183,644 | 158,546 (86%) | 25,098 (14%) |

It is worth noting that, under Article 17 of the Regulations Governing Securities Investment by Overseas Chinese and Foreign Nationals, foreign investors are required to designate a bank or securities firm approved by the Financial Supervisory Commission (FSC) as their custodian. The custodian is responsible for fund and securities safekeeping, trade confirmation, settlement, and data reporting. Accordingly, when foreign investors engage in securities lending transactions in Taiwan, they must conduct fund and securities custody and related cash management through their designated custodian. Payment of lending-related fees also requires prior instruction from the foreign investor, after which the custodian executes the fund transfer and subsequent payment according to such instructions.

This process involves multiple parties, including the foreign investor, the custodian, and other operational units, creating a pain point for foreign participation in Taiwan’s securities lending market. It increases communication and operational costs and complicates administrative procedures, affecting the timeliness and efficiency of payments. As the securities lending market continues to expand in scale and transaction frequency increases, the efficiency limitations of the current per-transaction processing model have become increasingly apparent. Consequently, recommendations from custodians and foreign investors to optimize the payment mechanism have become necessary to improve market operational efficiency and enhance convenience for international investors.

Key Analysis of Adjustments to Securities Lending Fee Payment Mechanism

To align with international market practices and optimize accounting processes for market participants, the TWSE announced on November 3, 2025, an adjustment to the payment mechanism for securities lending transaction fees. The adjustment aims to significantly reduce the frequency of fee payments for foreign investors’ negotiated transactions and enhance market efficiency. The adjustment is scheduled to take effect on June 1, 2026. Key points are as follows:

(1) Fee Payment Mechanism for Lending Transactions

For outstanding (unsettled) borrowed securities, fees will be calculated and paid monthly.

In the case of returned or partially early-returned securities: for negotiated transactions, fees will also be calculated and paid monthly; for fixed-price and competitive-bid transactions, the current practice remains, with fees paid on the next business day following the return of securities.

(2) Timing of Monthly Fee Settlement and Payment:

Fees will be calculated on the first business day of each month and completed for payment on the following business day.

Accordingly, whether for fixed-price, competitive-bid, or negotiated transactions, this adjustment focuses on outstanding securities, implementing a monthly settlement and payment mechanism. Through monthly centralized settlement, lenders and borrowers can periodically receive or pay the relevant amounts, helping improve predictability and stability of cash management. At the same time, this mechanism ensures that fee recognition aligns more closely with the accrual basis and period-matching principles, enhancing accounting consistency and accuracy.

For negotiated transactions, in cases of full return or partial early return of borrowed securities, the current practice of collecting lending-related fees on the next business day following the return will be replaced by a monthly centralized settlement and payment mechanism. This adjustment is expected to significantly reduce the accounting burden and payment frequency for market participants and intermediary institutions, thereby enhancing overall operational efficiency.

For fixed-price and competitive-bid transactions, due to differences in transaction mechanisms compared to negotiated transactions, the current per-return settlement process is maintained. Borrowers must deliver collateral to the TWSE for safekeeping, and the TWSE assumes a guarantor role, bearing the risk of unreturned securities or unpaid fees. Therefore, when borrowers return securities mid-month, the TWSE simultaneously returns collateral and collects associated fees on behalf of lenders, rather than applying monthly settlement. This ensures fees are collected timely and mitigates the risk of uncollected fees after collateral is returned.

Under the premise of balancing market efficiency and risk control, this adjustment to the securities lending fee payment mechanism simplifies operational processes, reduces administrative burden for participants and intermediaries, and, in the long term, strengthens compliance with accrual accounting and period-matching principles. It enhances the reasonableness and consistency of fee recognition, improves the quality of financial reporting, and promotes overall market efficiency and development.

| Transaction Type | Previous Mechanism | Announced on Nov 3, 2025, Effective June 1, 2026 |

| Fixed-Price & Competitive-bid – Borrowing Fees and Loan Service fees |

1. Total lending-related fees were collected and paid by the securities firm after the borrower returned the securities. 2. For partial early returns, fees incurred for the returned portion were settled on the next business day. |

1. Monthly Payment: The TWSE calculates the lending-related fees for outstanding borrowed securities as of the previous month on the first business day. The securities firm informs transaction parties, and fees are paid on the following business day. 2. Return Payment: When the borrower returns all or part of the securities early, the TWSE calculates fees for that portion, the securities firm notifies transaction parties, and fees are paid on the following business day. |

| Fixed-Price & Competitive-bid – Borrowing Fees and Loan Service fees Negotiated Transactions –Loan Service fees |

Borrowers who partially returned securities during the lending period were required to pay fees for the returned portion on the next business day. | When borrowers return all or part of the securities, fees for that portion are aggregated with the monthly calculation of fees for outstanding securities as of the previous month. The securities firm informs transaction parties, and fees are paid on the following business day. |

Conclusion – Continuously Enhancing Market Efficiency and Fostering a Foreign Investor-Friendly Environment

Through this adjustment to the securities lending fee payment mechanism, market participants in negotiated transactions can significantly reduce the frequency of fee payments. Even in cases of mid-month full or partial returns of borrowed securities, fees can be consolidated, settled on the first business day of each month, and paid on the following business day. By adopting a centralized processing mechanism, the previous multi-step handling process is effectively simplified, improving overall operational efficiency.

This adjustment not only reduces operational burden and communication costs, enhancing the stability of cash management, but also streamlines administrative procedures, lowers the risk of errors, and boosts market efficiency. In the long term, it contributes to the optimization of Taiwan’s securities lending market infrastructure, enhances the reasonableness and consistency of accounting treatments, and improves convenience and competitiveness for international investors. Consequently, it further strengthens the attractiveness and growth momentum of Taiwan’s capital market and achieves the policy goal of fostering a foreign investor-friendly investment environment.