I.Promoting Institutional Investors’ Implementation of Stewardship

Since the Taiwan Stock Exchange (TWSE) issued the Stewardship Principles for Institutional Investors in 2016, it has continuously encouraged institutional investors to closely monitor the operational performance of their investee companies. Through market mechanisms, the TWSE aims to enhance corporate governance standards, foster a virtuous cycle between institutional investors and investee companies, and ultimately increase the overall value of the capital market.

As of the end of December 2025, a total of 148 institutional investors have signed Taiwan’s Stewardship Principles, including 36 asset management firms, 39 insurance companies, 34 banks, 27 securities firms, 4 government funds, and 8 other institutions.

To further promote continuous improvement in the implementation of stewardship practices, the TWSE established the Stewardship Principles Advisory Committee in 2020 and introduced a public evaluation mechanism. Each year, the TWSE conducts an assessment to identify international standards better stewardship disclosure. In addition, to align the evaluation criteria with international standards and enhance their level of differentiation, the TWSE regularly reviews and revises the criteria by taking into account domestic and international stewardship trends, regulations, policies, and stakeholder feedback. These efforts aim to continuously strengthen both the practical implementation of stewardship and the quality of information disclosure among institutional investors.

II. Overview of the Implementation of the 2025 Stewardship Evaluation

(1) Overview of the Evaluation Criteria

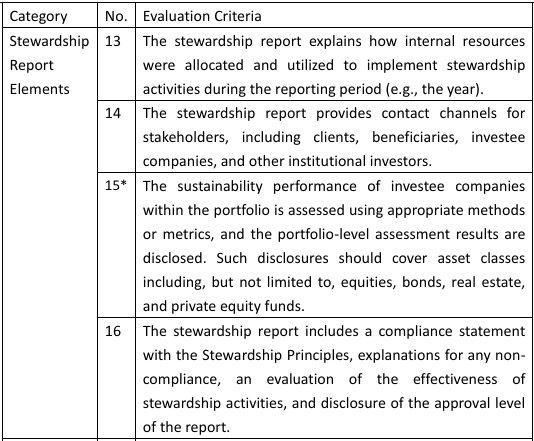

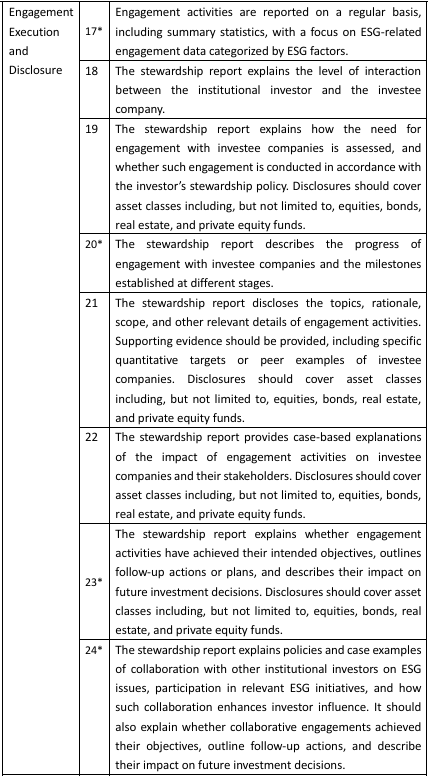

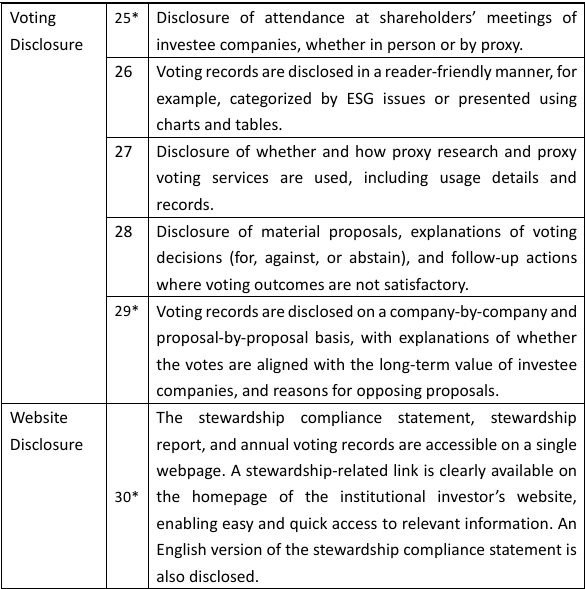

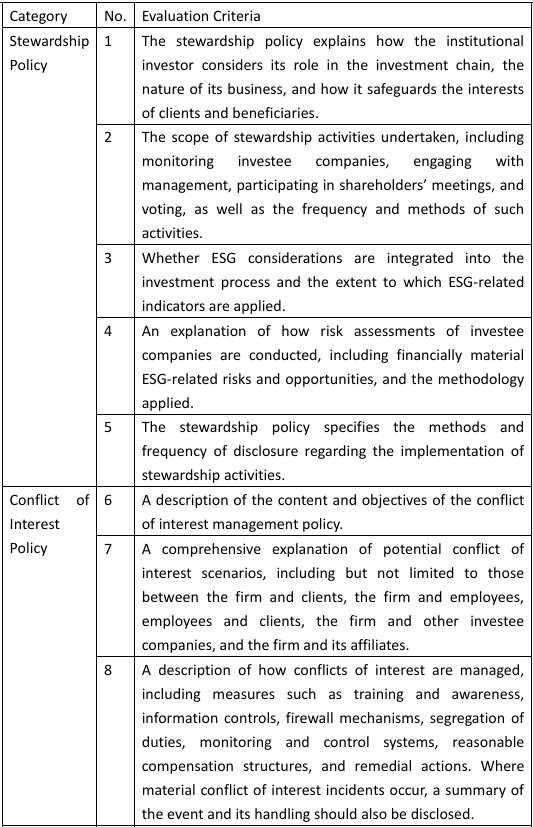

The 2025 evaluation framework is structured into two dimensions: (i) Policies and Compliance Statements and (ii) Practices and Disclosure, comprising a total of 30 evaluation indicators (see Appendix for details).

The former includes disclosures on stewardship policies, conflict of interest policies, and voting policies. The latter covers categories such as the key elements of stewardship reports, the execution and disclosure of engagement cases, voting disclosure, and website disclosure.

To enhance the discriminatory power of the evaluation criteria, the TWSE introduced a weighting mechanism starting from 2024. In light of the fact that most institutional investors have reached a relatively mature level in the Policies and Compliance Statements dimension in recent years, and that engagement practices and voting disclosure are key areas of international focus, the TWSE has retained the existing weighting structure in 2025 to further align Taiwan’s stewardship practices with international standards. The weighting for the first and second dimensions is set at 0.8 and 1.2, respectively.

(2) Scope of Evaluation and Institutions

The evaluation covers professional institutional investors that have signed the Stewardship Principles for Institutional Investors. Professional institutional investors are defined in accordance with Article 4, Paragraph 1, Subparagraph 1 of the proviso of the Financial Consumer Protection Act, and include both domestic and foreign institutions such as banks, securities firms, futures firms, insurance companies, fund management companies, and government investment institutions. The evaluation is conducted separately for domestic and foreign groups.

For the domestic group, the scope of evaluation includes stewardship activities conducted domestically or in relation to Taiwanese companies, as well as the corresponding disclosures. These institutions may appoint overseas affiliates or other professional institutions to carry out relevant activities and provide Chinese-language disclosures, including compliance statements, stewardship reports, and voting records. However, global stewardship information of overseas affiliates or professional institutions is excluded from the evaluation scope.

For the foreign group, the scope of evaluation includes the stewardship activities undertaken by the institutions and their related disclosures.

(3) Evaluation Timeline and Procedures

1. Submission of Stewardship Information

By the end of September 2025, evaluated institutional investors are required to disclose their annual stewardship activities (including stewardship reports and voting records) and related information on their corporate websites, and to submit relevant responses through the TWSE-designated online platform.

2. Evaluation Process

The Corporate Governance Center reviews the information disclosed on the websites of evaluated institutional investors and assigns scores based on the Evaluation Criteria for the Best Practice List of Stewardship Disclosure. Each indicator is rated as follows: 3 points (Grade A, best practice), 2 points (Grade B, acceptable), and 1 point (Grade C, needs improvement).

In addition, to encourage institutional investors to strengthen stewardship through concrete measures, eight indicators in the 2025 evaluation framework are designated as bonus items. Institutions that meet the criteria for Grade A in these items are awarded 4 points.

3. Committee Review and Publication of Results

In December 2025, the Stewardship Principles Advisory Committee convened to deliberate and finalize the annual list of institutional investors with better stewardship disclosure. The results were published on the Corporate Governance Center’s website on December 31, 2025, comprising 35 institutional investors in the domestic group and 5 in the foreign group.

III. Analysis of the 2025 Evaluation Results

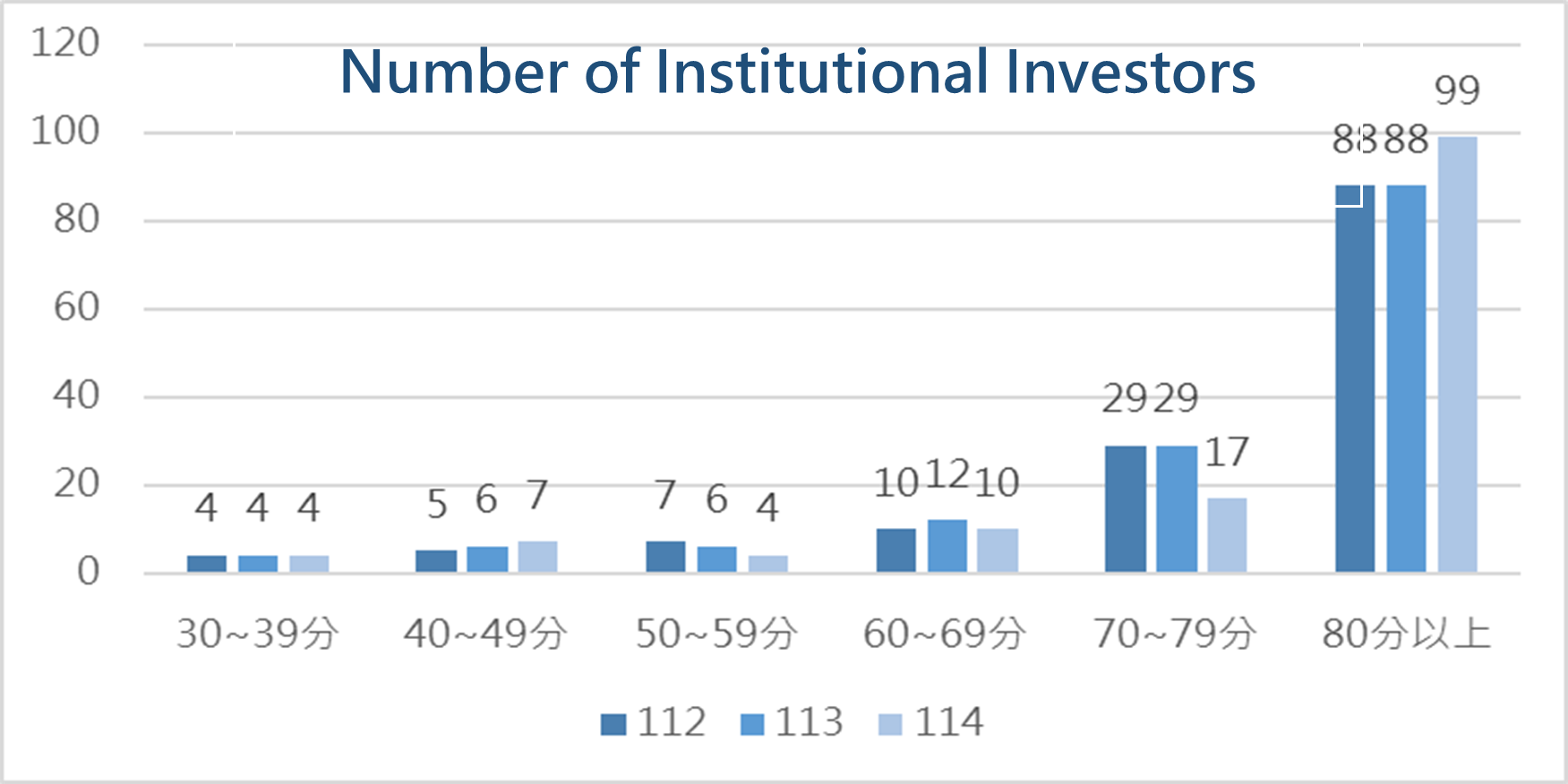

(1) Distribution of Scores of Domestic Institutional Investors Over the Past Three Years

Compared with the evaluation results in 2023 and 2024, institutional investors showed continued improvement across multiple evaluation criteria in 2025. Based on observations of the evaluation criteria, most institutional investors have gradually strengthened their stewardship-related policies. This year, a new criterion was introduced requiring an explanation of financially material ESG-related risks and opportunities, with the aim of encouraging institutional investors to provide a clearer description in their stewardship reports of how they identify, assess, and incorporate material sustainability issues that affect investment decision-making and risk management.

At the same time, in order to further align with international investors, the English version of the stewardship compliance statement was also included in this year’s evaluation criteria. The TWSE expects institutional investors to continue deepening their stewardship practices, particularly by making further improvements in the execution of engagement activities, the completeness of related disclosures, voting disclosure, and explanations of voting rationales, thereby enhancing the transparency of information disclosure and further strengthening the sound development of Taiwan’s capital market.

Overall, the number of institutional investors scoring 70 points or above reached 116, accounting for more than 80% of all evaluated institutions. This demonstrates that, under the evaluation mechanism, institutional investors have actively improved the quality of their disclosures and further advanced the implementation of stewardship practices.

(2) Key Areas of Strong Performance in 2025

Based on the 2025 evaluation results, the higher-performing indicators were largely concentrated in the Stewardship Policy category. These include criteria such as: institutional investors’ consideration of their role within the investment chain, the nature of their business, and how they safeguard the interests of clients and beneficiaries, the scope of stewardship activities undertaken, the methods and frequency of disclosure regarding the implementation of stewardship, and the content and objectives of conflict of interest management policies. These indicators generally received higher scores.

This outcome indicates that most institutional investors have achieved a relatively high standard in disclosing their stewardship policies. In particular, the overall quality of disclosure is well established in areas such as the nature of their business, their positioning within the investment chain, the methods used to disclose stewardship implementation, and the articulation of conflict of interest management policies.

In addition, a considerable proportion of institutional investors have also provided comprehensive disclosures on items such as the methods for managing conflicts of interest and voting policies, including principles for attending shareholders’ meetings (whether in person, via virtual attendance, or through electronic voting) or appointing proxies to exercise voting rights.

Overall, under the TWSE’s ongoing guidance and promotion in recent years, the stewardship-related policies established by institutional investors have become increasingly robust. The performance of the Policies and Compliance Statements dimension has also reached a relatively mature level.

(3) Areas for Improvement in 2025

The areas identified for improvement in the 2025 evaluation were primarily concentrated in the Policies and Compliance Statements dimension, particularly the newly revised and more substantive criterion on financially material ESG-related risks and opportunities, as well as in the Practices and Disclosure dimension, especially in categories related to engagement execution and disclosure and voting disclosure.

Overall, these areas largely pertain to the practical implementation of stewardship activities and the disclosure of related outcomes. Compared to policy-level disclosures, these criteria place greater emphasis on detailed methodologies, processes, and case-based explanations. As such, there remains room for further enhancement in practical application. The key observations from the 2025 evaluation are summarized as follows:

- The stewardship report explains how risk assessments of investee companies are conducted, including financially material ESG-related risks and opportunities, and describes the assessment methodology.

This evaluation criterion requires institutional investors to provide a comprehensive explanation of their risk assessment methodologies, with explicit reference to financially material ESG-related risks and opportunities. Observations indicate that most institutional investors have incorporated ESG factors into their investment decision-making processes or evaluation frameworks. However, some institutions have not sufficiently disclosed how they determine financial materiality or the underlying assessment framework. In addition, certain disclosures focus primarily on ESG-related risks without adequately addressing opportunities, resulting in comparatively lower scores. - The stewardship report explains how the need for engagement with investee companies is assessed, and whether such engagement activities are conducted in accordance with the investor’s stewardship policies.

This criterion requires institutional investors to outline their policies or evaluation processes for determining engagement with investee companies across different asset classes, and to explain whether engagement activities are aligned with their stewardship policies. Observations show that some institutions have not clearly articulated their assessment approaches or decision criteria across asset classes, nor have they sufficiently demonstrated how engagement activities are linked to their existing stewardship policies, leading to relatively lower evaluation results.

- The stewardship report discloses the topics, rationale, scope, and other relevant details of engagement activities with investee companies.

This criterion requires institutional investors to provide concrete evidence supporting their engagement activities, such as disclosing specific quantitative targets or case examples, including board gender diversity, greenhouse gas emissions, or instances of material non-compliance with sustainability principles by investee companies. Disclosures are also expected to meet cross-asset class requirements. In practice, some institutions provide insufficient information regarding the background of engagement topics, the rationale for engagement, the scope of interactions, or outcome indicators, and lack concrete case examples or quantitative data, resulting in relatively weaker performance.

- The stewardship report explains the impact of engagement activities on investee companies and their stakeholders.

This criterion requires institutions to provide case-based explanations of the impacts of engagement, including specific effects on investee companies and their stakeholders, such as shareholders, customers, suppliers, employees, and the general public. Observations indicate that some institutions have not comprehensively detailed the impacts on different stakeholder groups. In addition, as cross-asset class disclosure requirements were newly introduced for this item in 2024, there remains significant room for improvement overall.

- The stewardship report discloses material proposals, explains the rationale for voting decisions (for, against, or abstain), and outlines follow-up actions if dissatisfied with the voting outcomes.

This criterion requires institutional investors not only to disclose material proposals, but also to explain the criteria or internal processes used to determine materiality, as well as to provide clear rationales for voting decisions (for, against, or abstain). Furthermore, where investors are dissatisfied with voting outcomes, they are expected to disclose potential follow-up actions, such as continued engagement with the company, expressing shareholder views, or undertaking further monitoring measures. Observations indicate that while some institutions have disclosed material proposals and voting results, their explanations of materiality assessment processes, voting rationales, and follow-up actions remain relatively brief and do not fully demonstrate their stewardship decision-making processes, leading to comparatively lower scores.

Overall, the aforementioned criteria primarily relate to the practical implementation of stewardship activities and the disclosure of tangible outcomes by institutional investors. Compared to policy-level descriptions, these areas require more detailed articulation of methodologies, processes, and supporting case examples. Going forward, further enhancements in the disclosure of assessment methodologies, the provision of quantitative information and practical case studies, and the strengthening of cross-asset class disclosures would help improve the overall transparency and comparability of stewardship reports. Such improvements would also contribute to the continued advancement of the overall quality of stewardship disclosure among institutional investors in Taiwan.

IV. Illustrative Examples of Best Practice in Stewardship Reporting

This section compiles and presents selected examples of best practices from leading institutional investors in Taiwan, focusing on evaluation criteria identified as areas for improvement. These examples are intended to serve as references for market participants, with the aim of fostering peer learning and healthy competition, and further enhancing the quality of stewardship reporting among institutional investors in Taiwan.

(1) The stewardship report explains how risk assessments of investee companies are conducted, including financially material ESG-related risks and opportunities, and describes the assessment methodology.

OO Life Insurance has explicitly incorporated responsible investment principles into its investment management process and investment policies, requiring ESG considerations to be integrated into capital allocation decisions. By refining its investment processes and leveraging internal investment information systems alongside external research resources, ESG factors are embedded into investment decision-making. The company has also established its Stewardship Principles, under which stewardship activities are conducted to enhance investment value and promote the long-term interests of the company, policyholders, shareholders, and other stakeholders.

In addition, OO Life Insurance has established an ESG Risk Review Procedure, under which ESG performance must be considered when investing in equities and bonds. The company adopts a “comply-or-explain” approach and an escalation process as part of its ESG integration framework.

Incorporation of ESG considerations into the investable universe:

The investment team carefully evaluates the ESG performance of potential investment targets. When initiating new investments, the team must first determine whether a target falls within an exclusion list or a watchlist. Targets on the exclusion list are not eligible for investment. For those on the watchlist, the investment team is required to conduct enhanced due diligence, assess the company’s ESG risk management capabilities, prepare an evaluation report, and submit the case for internal review and discussion before inclusion in the investable universe. Continuous monitoring of ESG performance is also required to mitigate ESG-related risks.

Ongoing and periodic ESG monitoring of investment holdings:

The investment team primarily relies on MSCI ESG research to continuously monitor changes in the ESG performance of existing holdings, including listed equities, corporate bonds, financial bonds, and government bonds. Supplementary references include Taiwan Sustainability Ratings and Corporate Governance Evaluation data. When a company’s ESG performance deteriorates and it is placed on the watchlist, an assessment report must be prepared promptly to analyze the causes of the downgrade or negative events, as well as the company’s response actions. Appropriate risk management measures are then adopted, such as continued monitoring, position reduction, or suspension of further investment. In addition, a comprehensive ESG review of all holdings is conducted annually in September.

Consideration of financially material ESG risks and opportunities:

OO Life Insurance references data from MSCI ESG Research, under which governance is regarded as the core pillar of ESG and serves as the foundation for evaluating ESG performance across all industries using a consistent standard. The environmental and social dimensions are assessed in relation to industry-specific core business activities, with a focus on financially material risks and opportunities linked to operations. For example, in the semiconductor industry, water resource management is considered a financially material ESG risk, while clean technology development represents a financially material ESG opportunity.

The company evaluates each investee’s exposure to ESG risks and its risk management capabilities relative to industry peers, and assigns ESG ratings ranging from AAA to CCC. Companies rated “B” or “CCC” by MSCI ESG are placed on the watchlist and must undergo the ESG Risk Review Procedure before any investment can be made.

(2) The stewardship report explains how the need for engagement with investee companies is assessed, and whether such engagement activities are conducted in accordance with the investor’s stewardship policies.

OO Asset Management supports the responsible allocation of client assets through two primary stewardship approaches: providing insights during the research and investment decision-making process, and leveraging its influence to enhance the sustainability practices of investee or borrowing entities.

In line with its sustainable investment philosophy, the firm believes that more sustainable corporate behavior leads to stronger long-term financial outcomes. Accordingly, it has established a set of guiding principles and best practices, encouraging issuers to adopt them. These principles incorporate the concept of double materiality, requiring companies to understand and manage both their exposures and their impacts.

This section outlines the firm’s stewardship approach, including how it conducts corporate engagement and monitors progress across equities and fixed income, as well as the systemic sustainability themes that shape stewardship priorities, expectations toward companies, corporate governance and proxy voting practices, and stewardship-related disclosures.

Engagement with investee companies on ESG issues is considered a key driver of long-term sustainable development and positive investment returns. The firm’s engagement capabilities are grounded in its integrated fundamental research process, whereby analysis of material sustainability factors and engagement outcomes are incorporated into fundamental research and proprietary ESG ratings. This integration supports more informed investment decisions and improved investment outcomes, including enhanced operational performance and reduced cost of capital.

Identification of engagement opportunities:

The firm maintains ongoing dialogue with the management teams of investee companies. Portfolio managers and analysts regularly participate in formal meetings, typically held twice a year, to discuss company fundamentals. In addition to these regular interactions, ESG-related engagement opportunities arise in various contexts, including:

- Responding to controversies or adverse events, or concerns raised by analysts or portfolio managers (e.g., strategic or governance-related issues).

- Engagement initiated following ESG assessments, where analysts identify companies requiring further dialogue (e.g., emerging sustainability risks or weak performance on principal adverse impact indicators).

- Systematic and targeted engagement programs for companies held within sustainable investment products and strategies.

- Thematic engagement led by the sustainable investment team on specific sustainability issues, with topic selection based on urgency, alignment with the firm’s sustainability strategy, and input from clients and investment teams.

- Engagement requested by issuers in relation to specific corporate events (e.g., mergers and acquisitions or IPOs). Where material non-public information may be involved, the firm’s legal and capital markets teams provide support.

- Proactive engagement related to shareholder voting matters, including pre- or post-voting consultations with companies.

- In fixed income, engagement may occur prior to investment. For use-of-proceeds bonds, such as green or social bonds, engagement may be conducted to ensure responsible capital allocation. For sustainability-linked bonds, the firm may engage with issuers post-issuance to discuss KPIs, monitor progress, and encourage greater ambition in sustainability strategies.

Approach to corporate engagement:

Once engagement opportunities are identified, the firm emphasizes constructive dialogue with companies, clearly communicating its views and expectations to promote long-term behavioral change. Given its strong research capabilities and long-term investment orientation, OO Asset Management is able to engage deeply with global companies and build long-term relationships to drive meaningful ESG outcomes.

The firm believes that constructive engagement is often more effective than exclusion policies in driving change and delivering better outcomes for clients. Its engagement process is well-defined and transparent, incorporating clear objectives, milestones, timelines, and outcomes to measure progress. Key elements of the engagement framework include:

- Key issue areas: topics requiring improvement (e.g., climate change)

- Objectives: desired outcomes of engagement (e.g., reduction in carbon intensity)

- Milestones: indicators of progress toward objectives (e.g., setting emissions reduction targets)

- Key Performance Indicators (KPIs): measurable metrics aligned with milestones

- Timelines: expected timeframe for achieving improvements

- Status: progress assessment at a given point in time (e.g., no progress, partial progress, target achieved)

Monitoring progress:

Corporate engagement is an ongoing process of constructive dialogue. To monitor progress, all engagement activities are recorded in an internal research platform accessible to all investment teams. This high level of transparency enables cross-sector, thematic, and cross-asset insights, strengthening institutional knowledge. The duration of engagement varies depending on the materiality and urgency of ESG issues. Outcomes, or lack thereof, are reflected by analysts in ESG ratings, ensuring that engagement results are systematically integrated into investment assessments.

(3) The stewardship report discloses the topics, rationale, scope, and other relevant details of engagement activities with investee companies, and the stewardship report explains the impact of engagement activities on investee companies and their stakeholders.

| Theme |

Workforce Management; Human Rights Ongoing ESG Engagement |

| Level of Interaction | OO Asset Management Representatives: Fundamental Analyst; Sustainable Investment Analyst Company Representatives: Investor Relations Team; ESG Team |

| Asset Class Held | Equities |

| Milestone | Disclosure of the management framework for labor outsourcing providers |

| Engagement Details and Feedback |

In 2024, OO Asset Management’s fundamental analyst and sustainability analyst met with the investor relations and ESG teams of one of the world’s largest electronics manufacturers. We have engaged with this company for several years, and the objective of this meeting was to deepen our understanding of its labor and value chain management, particularly in response to recent allegations of discrimination in the recruitment process at one of its overseas factories. Given the company’s large workforce and its reliance on temporary contract workers during peak seasons, effective labor management is of critical importance. The company relies on labor outsourcing providers to deploy a substantial local workforce. In light of its past labor-related allegations, strong oversight and control mechanisms are essential to reduce operational and legal risks and to uphold labor rights standards across the value chain. During the discussion, the company provided additional information regarding local government inspections and its internal investigation in response to the allegations. It confirmed that labor outsourcing providers are audited annually and that whistleblowing channels are available for relevant parties to raise potential concerns. More importantly, the company is taking proactive steps to strengthen its broader ESG audit program. Key developments include:

We recommended that the company enhance transparency in its oversight of labor outsourcing providers by disclosing its audit systems, audit findings, and corrective actions, in a manner consistent with the rigor of its existing supplier management disclosures. In addition, due to the scale of its operations, the company has relatively high energy consumption. It has established clear targets to reduce total energy consumption and improve energy efficiency. The company has committed to achieving net-zero greenhouse gas emissions by 2050. This commitment includes interim targets, such as reducing absolute carbon emissions by 21% by 2025 and by 42% by 2030. It has also joined a collaborative initiative with the goal of using 100% renewable electricity across its global operations by 2040. In addition, the company has made progress on board gender diversity. The proportion of female directors increased from 10% in 2022 to 28.5% in 2024. The company aims to achieve more than 30% female board representation by 2025, and we will continue to monitor progress toward this target. |

| Impact on the Investee Company and Its Stakeholders |

|

| Follow-up Actions | We will continue to monitor the company’s progress. Future engagement will focus on the implementation of third-party operational audits and enhanced disclosure regarding the oversight of labor outsourcing providers. We will also continue to follow up on other ESG issues of concern. |

(4) The stewardship report discloses material proposals, explains the rationale for voting decisions (for, against, or abstain), and outlines follow-up actions where the voting outcomes are not satisfactory.

|

OO Life Insurance – Assessment of Material Proposals To safeguard client interests and promote the overall interests of shareholders, the company conducts a prudent assessment of whether proposals fall under the following two categories: Whether the proposals submitted to shareholders’ meetings or related meetings may have a material impact on the interests of the company’s clients or shareholders; (1) Abstention Policy Voting on the election of directors and supervisors: Exceptions apply in the following cases: Investments in public or social welfare enterprises in accordance with regulations governing the use of insurance funds; Proposals that may hinder the sustainable development or corporate governance of investee companies, or that may have significant adverse social impacts, will not be supported. The company will vote against proposals under the following circumstances:

|

|||

| Voting Position | Proposal | Rationale | Follow-up Actions (for Against Votes) |

| For | 2024 Business Report and Financial Statements | In the absence of concerns under the “Abstention Policy” or “Opposition Policy,” voting support is given in recognition of the investee company’s managerial expertise and to facilitate its effective development. | – |

| Against (Insufficient protection of shareholder interests) | Proposal to Delist and Terminate Public Company Status | The company intends to delist due to underperformance in operations, with the aim of facilitating internal operational and organizational restructuring. Management has indicated plans to reapply for public listing once operations improve. The proposal was approved, with more than two-thirds of the outstanding shares represented at the meeting voting in favor. | As the shares will become illiquid following delisting, the investment team will continue to monitor the company’s operational performance and will consider adjusting its position when the company relists or provides an opportunity for share disposal. |

| Abstain | Election of One Additional Director | In accordance with Article 146-1 of the Insurance Act. | – |

V. Conclusion

The results of the 2025 evaluation of institutional investors with better stewardship disclosure demonstrate both the importance that institutional investors attach to stewardship and their proactive efforts to enhance the quality of information disclosure. To foster a positive market cycle, the TWSE will continue to promote benchmarking and healthy competition through initiatives such as awareness seminars, the publication of disclosure recommendations, and the sharing of best practice examples, thereby supporting the enhancement of the international competitiveness of Taiwan’s capital market.

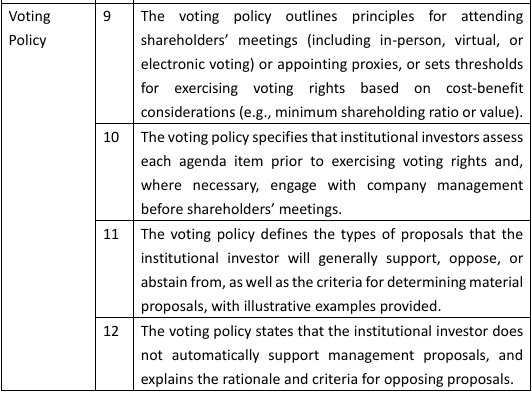

Appendix: Evaluation Criteria for the 2025 Best Practice List of Stewardship Disclosure

Dimension I: Policies and Compliance Statements

Dimension II: Practices and Disclosure