Introduction

In recent years, personal income and asset holdings in Taiwan have continued to grow—together with a prolonged global low-interest-rate environment and the diversification of financial products—investors have gradually shifted away from relying solely on individual financial products or short-term trading strategies. Instead, they are increasingly turning toward wealth management services including asset allocation and long-term financial planning. Following this trend, wealth management has become an important indicator of competitiveness in financial markets.

Within Taiwan’s financial system, banks have long played a dominant role in the wealth management market. By contrast, although securities firms possess strong expertise in capital markets, their entry into the wealth management sector occurred relatively late due to regulatory constraints. It was not until September 2009, when securities firms were permitted to conduct wealth management business through trust structures, that a significant breakthrough was achieved in the development of securities firms’ wealth management operations.

In 2024, the Financial Supervisory Commission (FSC) proposed five major initiatives aimed at positioning Taiwan as an “Asian Asset Management Center,” with the core objective of “retaining domestic wealth and attracting foreign capital.” Through regulatory easing and market revitalization, the policy seeks to transform Taiwan into an internationally competitive financial hub. In this context, the depth and breadth of wealth management services provided by securities firms—as key intermediaries in the capital markets—constitute a critical indicator of whether these policy objectives can be successfully achieved.

This article reviews the evolution of securities firms’ wealth management business, analyzes current growth trends, and summarizes the findings of a legal research project commissioned by the Taiwan Stock Exchange (TWSE) and conducted by Deloitte Legal. Based on these findings, the article presents policy recommendations and an outlook for future development.

Development Milestones of Securities Firms’ Wealth Management Business

On July 27, 2005, the FSC issued “the Directions for the Conduct of Wealth Management Business by Securities Firms” formally allowing securities firms to begin offering wealth management services. However, due to the absence of a trust framework and the inability of securities firms to control client cash flows, clients were required to open multiple accounts for different products. These structural limitations posed significant obstacles to the effective promotion of wealth management services.

To enable securities firms to provide clients with integrated accounts for asset allocation, the FSC opened the door on April 11, 2008 for securities firms to manage asset allocation through dedicated wealth management accounts. Subsequently, on September 28, 2009, securities firms were permitted to conduct wealth management business through pecuniary trust and securities trusts. Through the operation of trust accounts, securities firms could assist clients in investing across various financial products while simultaneously safeguarding investors’ rights and interests.

On August 28, 2014, the FSC amended relevant regulations to allow securities firms to conduct collective management trust business within client-designated operating scopes or methods. Upon obtaining regulatory approval, securities firms could pool trust funds with similar investment mandates into collective management accounts and manage them based on professional expertise and client needs.

In response to the growing demand for wealth management services among high-net-worth clients, the FSC announced regulatory amendments on September 8, 2020. These amendments relaxed restrictions on services provided to high-net-worth clients with investable assets exceeding NT$100 million, expanding the range of financial products accessible through sub-brokerage channels, wealth management channels, and proprietary trading at business premises.

Furthermore, the FSC has progressively expanded the scope of trust services that securities firms are permitted to conduct. For example, in 2016, securities firms were allowed to offer employee stock ownership trusts, employee welfare savings trusts, and insurance benefit trusts. In 2021, securities firms were permitted to conduct third-party beneficiary securities trusts—primarily principal-self-benefit and income-third-party-benefit structures—to assist clients with wealth and estate planning. In 2023, under the Trust 2.0 initiative, wealth management services were no longer limited to asset allocation; securities firms were allowed to offer client-oriented, integrated trust products, including elder-care trusts and education trusts, enabling comprehensive financial planning.

To align with the Asian Asset Management Center policy, the FSC issued the “Operating Principles for Financial Institutions Applying to Pilot Businesses in Local Asset Management Zones” on April 1, 2025. Under this framework, eligible securities firms operating within designated zones may offer high-net-worth clients a broader range of products and services to meet diversified asset management needs.

Current Status of Securities Firms’ Wealth Management Business

Since securities firms were permitted to conduct wealth management business through trust structures in 2009, eligible firms have gradually applied for approval. To date, ten securities firms—Uni-President, MasterLink, Mega, Cathay, Capital Securities, KGI, Hua Nan Yung Chang, Fubon, Yuanta, and SinoPac—have been approved to operate wealth management business via trust structures. In addition, MasterLink and Yuanta Securities have been approved to conduct discretionary investment management business through trusts.

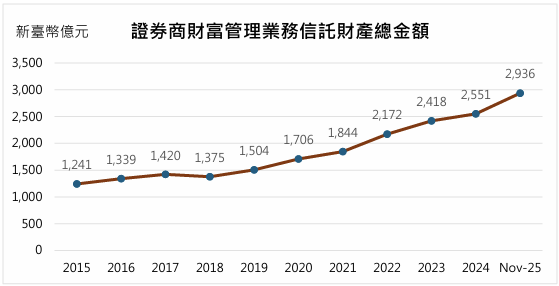

According to statistics published by the Securities Firms Association (as shown in the figure above), the scale of trust assets managed by securities firms increased from NT$124.1 billion at the end of 2015 to NT$293.6 billion by the end of November 2025, representing approximately a 2.36-fold growth over a ten-year period. However, as of the third quarter of 2025, the total size of trust property in Taiwan had reached NT$19.51 trillion. Of this amount, the combined total of pecuniary trust (excluding custody of securities investment trust and futures trust funds) and securities trust assets that securities firms are permitted to conduct amounted to approximately NT$9.35 trillion. Banks accounted for more than 90% of the market share in these two categories of trust business, while securities firms held only around 3%. As a result, securities firms continue to seek regulatory breakthroughs to expand opportunities in wealth management, with the aim of enhancing their competitiveness vis-à-vis the banking sector.

As of November 2025, pecuniary trust property totaled NT$264.3 billion, accounting for approximately 90% of total trust property, primarily invested in domestic securities investment trust funds (mainly money market and equity funds). Securities trust property totaled NT$29.2 billion, accounting for around 10%, with underlying assets mainly consisting of securities lending, allowing clients to enhance returns on long-term equity holdings.

Regulatory Frameworks for Securities Firms’ Wealth Management Business Abroad

To enhance the competitiveness of securities firms in wealth management, the TWSE commissioned Deloitte Legal between 2024 and 2025 to conduct a study titled “Legal Frameworks Governing Securities Firms’ Wealth Management Business”. The study analyzed wealth management regulations in key Asian markets—Singapore, Hong Kong, Japan, and South Korea—drawing on international practices and interviews with domestic securities firms to assess Taiwan’s current regulatory framework. The objective was to propose regulatory adjustments that would allow securities firms to expand wealth management services within controllable risk parameters, better respond to client needs, enhance competitiveness, and support the FSC’s Asian Asset Management Center policy.

【Singapore】

As a leading wealth management hub in Asia, Singapore’s regulatory framework centers on the “Securities and Futures Act” enacted in 2001. The Monetary Authority of Singapore (MAS) established an integrated and internationally competitive regulatory regime under this Act. Securities firms engaging in wealth management activities must obtain a Capital Markets Services (CMS) license. A key feature is that firms need not obtain multiple licenses based on corporate form; holders of a CMS license may engage in activities involving securities, collective investment schemes, over-the-counter derivatives, exchange-traded derivatives, and spot foreign exchange for leveraged trading.

Singapore adopts a “negative list” regulatory approach: unless expressly prohibited or subject to special approval due to high risk, licensed firms enjoy autonomy in product development and service provision, provided capital adequacy and risk management standards are met. MAS also promotes innovation through mechanisms such as regulatory sandboxes and the Variable Capital Company (VCC) structure, enabling rapid deployment of private equity and family office products.

Investor classification in Singapore includes Accredited Investors (AI), Expert Investors, and Institutional Investors. Individuals qualify as AIs if they possess net personal assets of at least SGD 2 million or annual income of at least SGD 300,000. Under the Opt-In Regime, eligible investors who voluntarily elect AI status waive certain investor protection provisions, allowing securities firms to offer highly customized, non-listed, and complex derivative products.

【Hong Kong】

Hong Kong’s wealth management regulatory framework is primarily governed by the “Securities and Futures Ordinance” implemented in 2003. The Securities and Futures Commission (SFC) emphasizes conduct regulation and suitability assessments, categorizing regulated activities into ten types (e.g., Type 1: Dealing in Securities; Type 4: Advising on Securities; Type 9: Asset Management). Securities firms typically require multiple licenses to conduct wealth management business, ensuring that each functional activity meets corresponding capital and responsible officer requirements.

The Professional Investor (PI) regime is central to Hong Kong’s thriving wealth management market. PIs are classified into institutional, corporate, and individual categories, with individual PIs required to hold investment portfolios of at least HKD 8 million. Licensed firms may offer PIs non-authorized investment products, including private funds, overseas property investment schemes, alternative investments, and unlisted structured products—enabling Hong Kong securities firms to compete directly with European and U.S. private banks.

Despite this flexibility, the SFC maintains stringent suitability requirements for the sale of complex products, including derivatives and non-exchange-traded structured products, ensuring that such products are appropriate for clients under all circumstances.

【Japan】

Japan implemented the “Financial Instruments and Exchange Act” in 2007, extending regulation from traditional securities business to comprehensive financial products. The regulatory framework emphasizes asset protection, requiring securities firms to strictly segregate client assets from proprietary assets, with custody typically entrusted to trust banks. Following the 2008 global financial crisis, this mechanism became a cornerstone of investor confidence in Japan’s wealth management services.

Recent regulatory revisions allow securities firms to act more freely as financial service intermediaries, facilitating agency sales of banking and insurance products and enabling one-stop wealth allocation services. Regulatory focus remains on transparency, with strict disclosure requirements for fees and conflicts of interest.

Japan operates a switching system between Professional Investors (Specified Investors) and General Investors. Specified Investors may access more complex and higher-risk products, while General Investors benefit from enhanced disclosure and product restrictions. Switching requires satisfaction of asset and knowledge thresholds and careful assessment by financial institutions.

【South Korea】

South Korea’s wealth management regulatory landscape underwent a major transformation with the enactment of the “Financial Investment Services and Capital Market Act” in 2009. The Act consolidated six previously separate laws covering securities, futures, and trusts, aiming to dismantle business barriers and cultivate large-scale investment banks. Under this framework, South Korea no longer maintains a concept equivalent to Taiwan’s “securities firm.” Financial investment companies licensed for trading or brokerage effectively perform functions similar to traditional securities companies.

Firms meeting capital and staffing requirements may concurrently engage in six major financial functions. This functional—rather than institutional—approach resembles Singapore’s model and is intended to foster “universal banking” capabilities.

A notable development is the liberalization of foreign exchange business. Restrictions on securities firms have been eased, allowing qualified firms to handle cross-border currency settlements and foreign-currency lending, significantly enhancing competitiveness in overseas wealth management.

Policy Recommendations and Outlook: Toward an Asian Asset Management Center

According to the study conducted by Deloitte Legal, Taiwan has made steady progress in opening diversified wealth management services for securities firms, with regulatory frameworks for investor protection and risk control generally well recognized by industry participants. However, from an international competitiveness and long-term market development perspective, existing regulations still lack sufficient flexibility and integration.

First, Taiwan continues to rely primarily on a positive-list regulatory model, under which securities firms may only conduct explicitly permitted businesses and must seek case-by-case approval for new products or services. While effective for ex-ante risk control, this approach is less flexible than the principle-based or negative-list models adopted by Singapore and Hong Kong. The study recommends considering a framework-based or negative-list approach, allowing innovation while maintaining investor protection.

Second, securities firms must currently apply for wealth management-related businesses on a product-by-product basis, resulting in complex approval processes and fragmented oversight. International markets have largely adopted integrated capital market frameworks that support one-stop, high-value wealth management services. The study suggests streamlining approval processes—for example, allowing branch-level trust services to be reviewed by the TWSE once headquarters approval has been granted—to enhance efficiency and competitiveness.

Third, investor classification mechanisms in Taiwan remain dispersed across different regulations, constraining the development of high-value wealth management services. The study recommends strengthening a tiered, investor-attribute-based supervisory framework, establishing clear identification mechanisms for high-net-worth and professional investors, and relaxing product access and sales restrictions for such investors based on assessed risk tolerance, while focusing supervisory resources on protecting retail investors.

Conclusion

Overall, Taiwan’s securities firms have achieved substantial progress in developing wealth management services. Future growth, however, hinges on a critical phase of institutional deepening and policy transformation. By enhancing regulatory flexibility and integration while maintaining robust supervisory foundations, securities firms can become significant wealth management providers alongside banks, leverage their capital market expertise, and serve as key drivers of Taiwan’s financial upgrading and international competitiveness.