The Rise of Active ETFs: Equity-Based Products Dominate Global Net Inflows

As a low-cost, transparent, and easy-to-trade investment vehicle, ETFs have long been favored by various types of investors. According to research firm ETFGI, as of the end of February 2025, the global ETF market had reached a record high of USD 15.5 trillion, over five times its size a decade ago. However, as market uncertainty increases, the limitations of traditional passive ETFs have become more apparent, driving growing interest in active ETFs. Although active ETFs still account for less than one-tenth of total ETF assets, their global AUM is growing at a much faster pace.

ETFGI data shows that active ETF assets first exceeded USD 100 billion in 2018 and had surged to a record USD 1.26 trillion by February 2025—30 times higher than a decade earlier, with a ten-year compound annual growth rate of 40.4%. By asset class, equity-focused active ETFs accounted for the majority of inflows. In February 2025 alone, global equity active ETFs saw net inflows of USD 25.07 billion, bringing the YTD total to USD 51.46 billion. Fixed income active ETFs attracted USD 22.13 billion in February, with a YTD total of USD 43.54 billion.

The U.S. market remains the most active in developing active ETFs. The world’s first active ETF was launched in the U.S. in 2008, and growth remained modest until the U.S. Securities and Exchange Commission (SEC) introduced ETF Rule 6c-11 in 2019. This rule simplified operational procedures and lowered costs by allowing eligible ETF issuers (including both passive and active ETFs) to launch funds without seeking individual exemptive relief from the SEC. It also removed quantitative constraints on portfolio components, such as market capitalization or liquidity thresholds. This rule paved the way for active ETFs, unlocking product innovation and marking a critical turning point for global expansion.

By integrating active management strategies with the ETF structure, active ETFs offer flexibility and agility in implementation. They have launched a wave of global investor interest and are transforming the asset management landscape. This article explores the development, regulatory reform, changing investor behaviors, and future trends of active ETFs across the U.S., Europe, and Asia-Pacific.

From Passive Tracking to Active Selection: Key Differences between Active and Passive ETFs

The primary distinction between active and passive ETFs lies in their management approach. Active ETFs are led by portfolio managers who actively adjust holdings based on market research and analysis, without tracking a specific index or benchmark. Their goal is to outperform benchmarks or achieve specific investment objectives. In contrast to passive ETFs, which replicate the performance of an index, active ETFs allow managers greater flexibility in portfolio decisions. While active ETFs face their own set of challenges, their adaptability allows them to seek out optimal opportunities under varying market conditions.

Passive ETFs are designed for investors seeking low-cost exposure to the broader market. They replicate index components to deliver market returns. In contrast, active ETFs appeal to investors who believe that active management can generate excess returns and are willing to pay slightly higher fees for that potential. The popularity of active ETFs has been steadily rising across global markets.

In positioning terms, active ETFs sit between passive ETFs and traditional actively managed mutual funds. Traditional mutual funds are also actively managed, aiming to outperform the market but often come with higher fees. On the other hand, proponents of passive investing argue that fully replicating market indices helps eliminate human error and delivers more cost-effective long-term results—highlighting the fee and simplicity advantages of passive ETFs.

However, active ETFs are gradually changing how investors approach market participation. These products combine the strategic stock selection of mutual funds with the liquidity, transparency, and cost efficiency of ETFs, making them an increasingly favored option. On the supply side, asset managers are also adopting ETFs as a preferred structure to execute public market strategies.

Originally, ETFs were designed to track specific indices, emphasizing low fees, high transparency, and intraday liquidity. But with the rapid evolution of global financial markets in the 2020s—including geopolitical risks, shifting monetary policies, and inflationary pressures—investors have sought tools capable of navigating volatility and generating alpha. Positioned between mutual funds and traditional ETFs, active ETFs strike a balance between strategic flexibility and trading efficiency, making them a key asset allocation tool for the new generation.

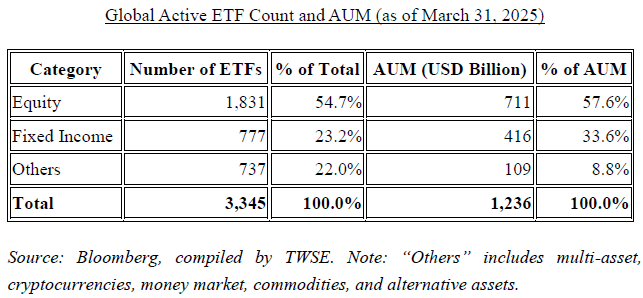

Overview of Global Active ETF Issuance: Equity-Based Products Maintain Dominant Position

As of March 31, 2025, there were 3,345 active ETFs globally. Among these, equity-based active ETFs accounted for the largest share with 1,831 products—54.7% of the total. Fixed income active ETFs totaled 777 (23.2%), while the remaining 737 (22.0%) fell into other categories such as multi-asset, cryptocurrency, money market, commodity, and alternative asset ETFs.

In terms of AUM, the total market value of global active ETFs was approximately USD 1.24 trillion. Equity active ETFs dominated with USD 711 billion in assets, representing 57.6% of the total. Fixed income active ETFs followed with USD 416 billion (33.6%), and other types held USD 109 billion (8.8%).

Overall, both in number and in total assets, equity-based active ETFs constitute the mainstream, reflecting their central role in investor portfolio allocations and product design strategies.

U.S. Market: Regulatory Relaxation and Product Diversification Drive Growth

I. Market Structure Evolution: Regulation Spurs Expansion

The U.S. introduced the world’s first active ETF in 2008. In 2019, the SEC passed ETF Rule 6c-11, which significantly lowered barriers for entry by allowing qualified ETF issuers—both passive and active—to launch products without seeking individual exemptive relief. This rule encouraged more issuers and investors to participate in the active ETF market. As a result, in 2020, newly launched active ETFs in the U.S. outnumbered passive ETFs for the first time, reflecting a major shift in market structure. This transformation was further accelerated during the COVID-19 pandemic, as investor demand surged for risk-managed and innovative strategies. ARK Invest’s flagship active ETFs (e.g., ARKK), which focus on disruptive innovation, gained significant attention during the pandemic. These funds employed active stock selection to target high-growth companies like Tesla, Roku, and Teladoc, drawing substantial retail inflows and broadening investor awareness of active ETFs.

As of February 2025, U.S. active ETF AUM had approached USD 1 trillion. Although this represents only about 8% of the U.S. ETF market—still well below the passive segment—its growth rate outpaces the broader ETF market. Between 2023 and 2024, 75% of newly listed ETFs in the U.S. were actively managed, highlighting strong investor interest in active strategies. This growth momentum stems from increased market volatility, driving investor demand for better risk management and alpha generation. Investors believe active fund managers are better equipped to navigate complex environments and outperform benchmarks.

II. Diverse Product Types: Equity Active ETFs Dominate

In terms of asset class, equity-focused active ETFs form the bulk of the U.S. market. These typically target large-cap stocks, growth stocks, dividend yield strategies, and ESG themes. Major asset managers—including BlackRock, State Street, Invesco, and disruptors like ARK Invest—have all made significant active ETF investments. For instance, ARK’s ARKK ETF, despite its high volatility, gained traction among retail investors post-pandemic due to its thematic focus and stock-picking prowess.

On the strategy side, defensive products such as Buffer ETFs and Derivative Income ETFs have also drawn investor attention. Buffer ETFs use options strategies to provide downside protection within preset limits, while capping upside gains. According to State Street’s 2025 Global ETF Outlook, Buffer ETFs were among the most prominent product strategies in 2024. Fund managers launched various structures featuring different protection levels and durations. Often referred to as "target outcome ETFs," these products are popular among investors looking to hedge bear markets or preserve capital later in life. Interestingly, younger investors are also increasingly turning to such protective instruments.

Derivative Income ETFs, such as JP Morgan’s JEPI, combine a portfolio of equities with a covered call strategy to generate income, offering relatively stable cash flow. These ETFs have gained popularity in environments of rising interest rates and market volatility. State Street expects continued growth in this segment in 2025, with increased product variety and broader issuer participation helping to diversify asset flows beyond the largest fund houses.

Disclosure has long been a focal issue for regulators and asset managers regarding active ETFs. Traditionally, ETFs are required to disclose full holdings daily. However, active strategies are more prone to being copied or front-run by the market, prompting some issuers to push for relaxed transparency requirements.

In 2019, the SEC approved Precidian Investments’ ActiveShares model, which introduced the Non-Transparent Active ETF structure. These ETFs are not required to publish their full holdings daily. In 2020, the SEC also approved semi-transparent models such as Blue Tractor’s structure, which allows the daily disclosure of a “tracking basket” partially overlapping with the fund’s actual holdings.

These semi-transparent ETFs offer a balance between protecting proprietary strategies and ensuring investor confidence. However, broad market acceptance remains limited. Most investors and platforms still prefer full-transparency active ETFs that publish daily holdings, citing greater trust and liquidity benefits.

European Market: Regulatory Liberalization and Product Innovation in Tandem

I. Growth Recovery and Market Characteristics

According to State Street research, starting in 2019, Europe began experiencing growth in active ETFs similar to the U.S. The momentum continued into 2024, with a notable surge in capital inflows and an expanding roster of products and issuers.

In 2024, the European ETF market regained strength, attracting a record USD 270 billion in net inflows. Active ETFs alone saw inflows jump from USD 7 billion in 2023 to USD 20 billion in 2024. The number of newly listed active ETFs increased from 103 to 178, while the number of issuers rose from 28 to 35—evidence of rising demand and growing supply on the product side. State Street expects this growth momentum to continue in 2025, with active ETFs maintaining a high share of newly listed products in Europe.

European active ETFs span diverse strategies—including equity, fixed income, thematic, and enhanced index ETFs—and are increasingly favored by traditional active managers such as J.P. Morgan, Janus Henderson, and Robeco. Morningstar research indicates that J.P. Morgan has solidified its lead as the top issuer of active ETFs in Europe, holding a 54.6% market share.

II. Regulatory Breakthrough: Luxembourg Leads the Way for Active ETFs

Initially, Europe's active ETF development lagged due to regulatory hurdles and conservative investor preferences. However, the EU is actively promoting financial innovation and deregulation. As Europe’s largest center for active fund management and the second-largest ETF domicile, Luxembourg has introduced several measures to make active ETF issuance more attractive:

- On December 11, 2024, Luxembourg's Parliament passed Bill No. 8414, which exempts active ETFs from subscription tax starting in 2025. The new rule extends the tax exemption already enjoyed by passive ETFs to active ones.

- On December 19, 2024, the Luxembourg financial regulator CSSF issued a FAQ document allowing delayed disclosure of active ETF holdings, requiring publication only once per month at minimum. This new transparency regime provides protection for active strategies.

- Luxembourg has also implemented a streamlined and efficient ETF approval process.

In addition, Luxembourg allows asset managers to launch “active ETF sub-funds” or “ETF share classes” under existing UCITS (Undertakings for Collective Investment in Transferable Securities) structures. This enables a single legal fund to offer both mutual fund shares and ETF shares. This structure helps reduce regulatory reporting, product development, and operational costs, thereby enhancing efficiency.

The UCITS framework, which comes with EU-wide passporting rights, combined with the tradability of ETFs, allows fund managers to broaden investor access through both platforms and exchanges. For asset managers looking to enter the European ETF market—especially in the active space—Luxembourg offers a regulatory advantage. Major global asset managers such as J.P. Morgan and Morgan Stanley have already adopted this model, listing ETF share classes on European exchanges. Their participation underscores both the viability and acceptance of the structure.

III. Retail Participation Rises and New Investment Channels Emerge

State Street research shows that retail participation in ETFs continues to rise across Europe. The number of participants in ETF savings plans—similar to Taiwan’s regular investment plans—rose from about 7.7 million in 2023 to 10.8 million in 2024, a growth rate exceeding 40%. Germany, France, and Belgium led the way, underscoring ETFs’ growing appeal as long-term wealth management tools.

According to Brown Brothers Harriman’s (BBH) 2025 Global ETF Investor Survey, many ETF issuers view Europe as a promising growth market. Over the next several years, Europe is expected to become a key growth driver. Factors contributing to this potential include increasing retail participation, advancements in digital trading infrastructure, and proactive investor education by new market entrants. Together, these elements are expected to usher in a new wave of growth for Europe’s ETF industry.

Asia-Pacific Market: Regional Development and Policy Advancements in Tandem

I. Overall Growth and Market Differentiation

According to research from State Street, the global ETF market continues to expand, with growth in the Asia-Pacific region outpacing that of North America and Europe. In 2024, the Asia-Pacific ETF market achieved an impressive 47% year-on-year increase in assets under management (AUM). This remarkable growth reflects both investor enthusiasm for ETF products and the rapid development of active ETFs. State Street projects another 30% increase in regional ETF AUM in 2025, with active ETFs playing a key role.

Since Australia launched its first active ETF in 2015, the Asia-Pacific region has gradually opened up to localized product innovation. South Korea began permitting active ETF issuance in 2017; China approved its first active ETFs in 2021; Hong Kong and Japan introduced actively managed ETF mechanisms in 2023; and Taiwan officially entered the market in 2025. These developments illustrate that Asia-Pacific markets are building distinctively localized active ETF product lines while attracting global issuers. Although still in an early stage, the region is expected to welcome a wave of differentiated and highly active ETF products that will deepen and broaden the market.

Among regional markets, South Korea stands out as having one of the highest active ETF penetration rates globally, with active ETFs accounting for more than 31% of its total ETF AUM. Despite political turmoil and a 10% drop in the KOSPI index in 2024, South Korea’s ETF market attracted USD 61 billion in inflows, driving a 58% year-on-year increase in total ETF market size. This growth was largely driven by retail participation and continued demand for active ETF products. According to State Street, the share of ETFs in South Korea’s total mutual fund market rose from 9.5% in 2022 to 15.5% in 2024. The expansion of active ETFs is increasingly encroaching on the space traditionally occupied by actively managed mutual funds. This shift reflects the appeal of ETFs’ lower expense ratios, intraday trading convenience, and highly digitalized investment channels.

II. Taiwan’s Market: Regulatory Breakthroughs Fuel the Takeoff of Active ETFs

Taiwan has emerged as one of the world’s fastest-growing ETF markets and currently ranks as the third-largest in Asia by AUM, behind only Japan and China. As of April 2025, Taiwan had 280 ETFs, with 181 listed on the TWSE and 99 on the OTC market. The total market size reached NT\$6.4 trillion—NT\$3.6 trillion on the TWSE and NT\$2.8 trillion on the OTC. In 2024 alone, the market expanded by 65%, a sharp rise compared to 2023 and approximately 38 times larger than a decade ago (when it stood at NT\$167.1 billion). This far exceeds the global average growth rate, indicating strong local acceptance and participation in ETF investment.

This rapid growth is driven not only by investors’ growing sophistication in asset allocation and cost sensitivity but also by regulatory liberalization and institutional innovation. In late 2024, the Financial Supervisory Commission (FSC) officially approved the launch of active ETFs and multi-asset passive ETFs in Taiwan, injecting new product variety and strategic flexibility into the market. This policy change has opened the door for innovation and is expected to attract more domestic and foreign capital.

On May 5, 2025, Taiwan’s first active ETF—the "Nomura Taiwan Smart Select Active ETF"—was officially listed. As an equity-focused active ETF, it marked Taiwan’s entry into the era of actively managed ETFs. It is expected that at least five domestic asset management firms will submit applications to launch their own branded equity active ETFs in 2025, featuring diverse stock selection strategies and industry themes. With the continued rise of fintech applications, widespread adoption of mobile trading platforms, maturing of regular investment mechanisms, and increasing participation by younger investors and long-term capital, active ETFs are poised to become a major growth driver for Taiwan’s ETF market.

Overall, backed by regulatory innovation, rising demand, and strong technological infrastructure, Taiwan’s ETF market is rapidly entering a new phase of diversification and internationalization. The introduction of active ETFs will further enhance the competitiveness and flexibility of Taiwan’s capital markets.

Investor Behavior Shift: From Passive Exposure to Strategic Rebalancing

As market volatility intensifies and investment strategies diversify, global investors are undergoing a structural behavioral shift. They are moving away from relying solely on low-cost, passive index-tracking ETFs and increasingly incorporating strategy-oriented active ETFs into their portfolios. This trend reflects rising demand for adaptability and risk control, and it signals that active ETFs are evolving from a niche alternative into a mainstream portfolio component.

I. Growing Acceptance of Active ETFs

According to BBH’s *2025 Global ETF Investor Survey*, 97% of respondents indicated plans to increase their allocation to active ETFs in 2025—evidence that this product category is entering a phase of rapid growth. The appeal of active ETFs is particularly pronounced in the U.S. and Greater China, where 36% and 29% of investors, respectively, stated they would significantly boost their active ETF holdings.

Several key factors are driving this surge in acceptance. On one hand, concerns over market uncertainty and heightened volatility have prompted investors to seek tools with built-in strategic and defensive features. On the other hand, investors are increasingly recognizing the value of active management in capturing specific market opportunities, adjusting allocations proactively, and potentially enhancing long-term returns. The BBH survey also found that investors are willing to pay slightly higher fees for access to professionally managed strategies and more transparent portfolio disclosures.

II. Capital Reallocation: From Passive ETFs and Mutual Funds to Active ETFs

This shift in investor preference is accompanied by real changes in capital allocation. According to the survey, 53% of respondents said they plan to reduce allocations to passive ETFs in favor of active ETFs. Similarly, 48% intend to reallocate funds from actively managed mutual funds or separately managed accounts (SMAs) into active ETFs.

This trend of portfolio rebalancing underscores a growing emphasis on strategic content, risk-hedging mechanisms, and transparency of performance. In an environment defined by heightened market uncertainty, active ETFs—especially those with thematic or tactical investment orientations—are becoming a focal point for capital flows.

III. Top Reasons for Choosing Active ETFs: Institutional Strategies and Risk Mitigation

Among the various reasons for choosing active ETFs, the top three cited by investors were: access to institutional-grade strategies (25%), high portfolio transparency (21%), and exposure to specific markets or themes (21%). This suggests that active ETFs are no longer seen merely as substitutes for mutual funds, but rather as integral tools for strategic asset allocation.

Notably, “cost” has dropped from the top of the list to the eighth position in terms of selection criteria. This shift indicates that investors are no longer fixated on minimizing fees alone; instead, they are willing to pay for higher-quality strategies and operational flexibility. This changing investor mindset poses a new challenge for ETF issuers: how to retain the structural advantages of ETFs (e.g., liquidity, transparency) while delivering differentiated active strategies. This will be a critical factor in future market competition.

Future Outlook: Strategic Diversification and Structural Innovation Will Drive Growth

As global capital markets undergo structural transformation and investment technologies continue to evolve, active ETFs are transitioning from a product concept to a strategic platform. In the coming years, innovation in strategies, breakthroughs in regulatory frameworks, and the integration of financial technology are expected to be the three core engines propelling active ETFs into a phase of accelerated development. These products are no longer simply an "extension of ETFs," but are emerging as a central hub in the transformation of asset management.

I. Strategy Expansion and Asset Class Diversification

The strategic layout of active ETFs is rapidly expanding across multiple asset classes, moving beyond traditional equity selection to display unprecedented diversity and professional depth. According to State Street, the total AUM of active fixed income ETFs in the U.S. doubled in 2024, reaching USD 282 billion. Among these, “multi-sector bond strategies” and “core bond allocations” were particularly favored by institutional investors, underscoring the growing demand for active management in fixed income.

Another key development is the rise of private asset ETFs. For instance, the SPDR SSGA Apollo IG Credit ETF combines listed credit instruments with private debt, breaking through the traditional limitations that have kept private investments out of ETF structures. This innovation enhances liquidity while opening a new chapter in the “commoditization” of private markets, carrying significant implications for the future of asset management.

Additionally, after the SEC formally approved spot bitcoin ETFs in 2024, the crypto ETF market rapidly expanded, with total AUM reaching USD 118 billion. As regulatory clarity improves, crypto ETFs are expected to evolve from single-coin exposure (e.g., bitcoin) to diversified portfolios incorporating futures, options, and other derivatives—ushering in a new wave of product innovation.

II. Structural Reform and Regulatory Breakthroughs

The ETF share class model (ETF and mutual fund co-structure) is currently one of the most closely watched innovations in the U.S. ETF market. This structure allows a mutual fund to issue ETF shares, or an ETF to issue mutual fund shares, enabling both vehicles to share the same investment portfolio while offering investors more options in terms of liquidity and convenience.

As of early 2025, over 40 asset management firms had submitted applications for ETF share class structures to the SEC, and the number continues to rise. Notably, approximately 74% of applications originate from active funds, while 26% come from passive ones—indicating particularly strong demand from active managers. The model is seen as a major innovation for expanding investor choices, reducing costs, and improving tax efficiency. However, challenges remain in terms of regulation and distribution. Whether the SEC will approve the structure, and how it will be implemented in practice, remains to be seen.

The potential of active ETFs also depends on structural regulatory innovation. The industry expects the SEC to approve the ETF share class structure by 2026. If so, mutual funds could convert into ETFs via share class conversion without requiring liquidation or restructuring. This would significantly lower transition costs and improve capital efficiency, unlocking the potential for thousands of mutual funds to become ETFs and massively increase the supply of active ETF products.

In Europe, Luxembourg—Europe’s largest center for active fund management and second-largest ETF registration jurisdiction—announced in late 2024 that it would ease rules on portfolio transparency and multi-share class structures for active ETFs. These changes enable more active strategies to list and trade in ETF format, and they are also attracting U.S. and Asian managers to migrate active strategies into UCITS structures. The policy shift is expected to accelerate cross-border issuance and global expansion.

These regulatory revisions and structural innovations not only offer favorable conditions for the growth of active ETFs but also reflect increasing regulatory confidence and recognition of this product type.

III. Education and Platform Support

Beyond regulation and strategy, investor education and platform infrastructure will be key drivers of active ETF adoption. With the growing popularity of automated investment plans, the maturation of robo-advisory platforms, and the integration of ETFs into digital brokerage interfaces, retail investors now face significantly lower barriers to entry. Active ETFs are no longer solely tools for institutional players—they are becoming integral to personal wealth management strategies.

In the future, active ETFs will increasingly incorporate artificial intelligence (AI), big data analytics, factor modeling, and ESG scoring systems to develop dynamically adjusted portfolios. Investment platforms will assist users with tools such as quantitative risk monitoring, personalized recommendation algorithms, and multi-factor screening, enabling them to construct ETF portfolios tailored to individual risk profiles and financial goals. Active ETFs will evolve beyond mere products into the central nervous system of digital wealth management.

Conclusion: Active ETFs Enter a New Phase of Maturity, Globalization, and Strategic Centrality

The rapid rise of active ETFs has gone far beyond serving as a temporary solution to market volatility. It now represents a profound transformation in the structure of the asset management industry. Their emergence signals a shift in industry focus—from scale-driven to strategy-driven, from efficiency-focused to tech-enabled paradigms. Over the past decade, the ETF market has largely been dominated by passive investing. Today, however, active ETFs have embedded themselves into core portfolios and are reshaping traditional views on asset allocation and risk management through their transparency, strategic flexibility, and technological integration.

The momentum behind this transformation stems from multiple converging forces. On one hand, deregulation and supervisory innovation have enabled active strategies to operate more efficiently within the ETF framework. For example, the proposed ETF share class reform in the U.S., expected by 2026, would allow mutual funds to convert to ETFs without liquidation or restructuring—providing robust institutional support for active expansion. On the other hand, Luxembourg has relaxed disclosure rules and UCITS structure constraints, accelerating the cross-border issuance and innovation of active ETFs in Europe. Meanwhile, Asian markets such as Taiwan are also embracing the active ETF model, pushing the global market toward greater diversity and internationalization.

In terms of product design, active ETFs have evolved well beyond simple stock-picking models. Today, they cover a wide spectrum—from basic covered call strategies and multi-asset allocations to ESG-themed funds and sophisticated hybrid models that blend quantitative algorithms with discretionary management. These innovations not only address different investor risk profiles but also extend ETF exposure into non-traditional areas such as private credit and cryptocurrencies, redefining both the breadth and function of the ETF universe.

Equally important are the unique advantages of active ETFs: daily holdings disclosure and intraday exchange trading. These features provide high transparency and liquidity, reinforcing market order and price efficiency. However, increased transparency also invites heightened scrutiny and performance accountability. For active ETF portfolio managers, the challenge lies not merely in tracking the market, but in demonstrating consistent strategy effectiveness and risk control amid volatility and thematic shifts—justifying the relatively higher fees through credible performance.

From an investor perspective, BBH’s 2025 survey reveals that 97% of respondents plan to increase active ETF allocations, with especially strong interest in the U.S. and Greater China. This shift not only affirms the perceived value of active management but also reflects a broader evolution in asset allocation—from a singular focus on cost efficiency to a more nuanced pursuit of strategy quality, risk control, and return potential. "Fees" are no longer the primary factor in ETF selection, now ranked eighth, highlighting that strategy and transparency have become the true drivers of investor behavior.

Fintech integration is also a defining force for the future of active ETFs. AI-powered stock selection engines, big data analytics, ESG scoring systems, and intelligent advisory platforms are accelerating the convergence of active strategies with digital tools. Active ETFs are no longer just financial instruments—they are becoming the strategic core of the digital wealth management ecosystem. For the next generation of investors, active ETFs offer programmable, real-time, and personalized strategy execution, enabling them to manage risk and seize opportunity in an ever-changing environment.

Looking ahead, the line between active and passive will continue to blur. Passive ETFs will remain a foundational, low-cost tool for market exposure, while active ETFs will become the engine for generating alpha through strategic adaptability and deep asset penetration. The future trajectory of ETFs will depend on whether the market continues to demand higher standards for performance, transparency, and value creation.

The evolution of active ETFs is not just about product innovation—it represents a fundamental reshaping of investment logic and asset management philosophy. In this strategic realignment of the industry, active ETFs are no longer a peripheral choice—they are becoming the core force driving global capital flows, asset allocation, and market efficiency, ushering in a new era of maturity, globalization, and strategic advancement in financial markets.